M&A Insurance: PE Quarterly Market Update – Q2 2022

Buy and Build Strategies Fuel Last Quarter M&A Growth M&A Insurance: Quarterly Market Update – Q2 2022

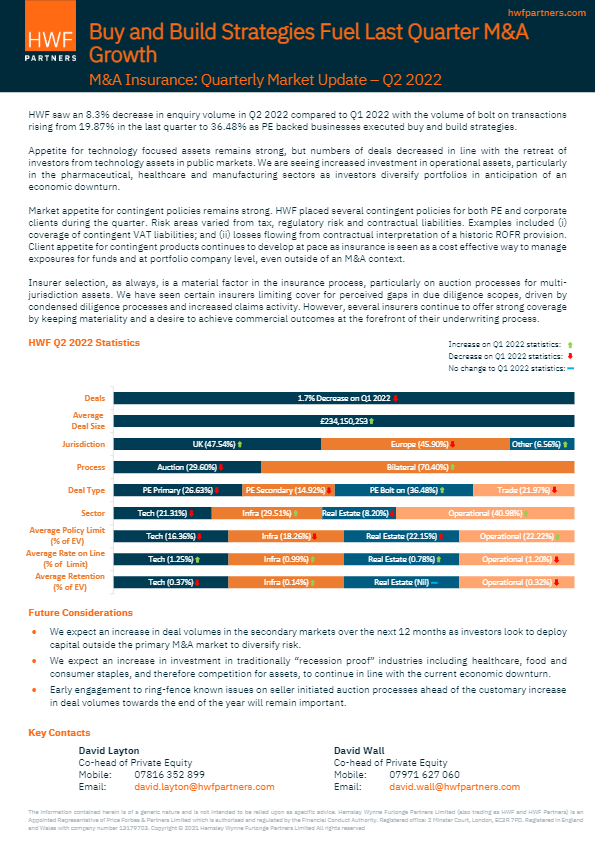

HWF saw an 8.3% decrease in enquiry volume in Q2 2022 compared to Q1 2022 with the volume of bolt on transactions rising from 19.87% in the last quarter to 36.48% as PE backed businesses executed buy and build strategies.

Appetite for technology focused assets remains strong, but numbers of deals decreased in line with the retreat of investors from technology assets in public markets. We are seeing increased investment in operational assets, particularly in the pharmaceutical, healthcare and manufacturing sectors as investors diversify portfolios in anticipation of an economic downturn.

Market appetite for contingent policies remains strong. HWF placed several contingent policies for both PE and corporate clients during the quarter. Risk areas varied from tax, regulatory risk and contractual liabilities. Examples included (i) coverage of contingent VAT liabilities; and (ii) losses flowing from contractual interpretation of a historic ROFR provision. Client appetite for contingent products continues to develop at pace as insurance is seen as a cost-effective way to manage exposures for funds and at portfolio company level, even outside of an M&A context.

Insurer selection, as always, is a material factor in the insurance process, particularly on auction processes for multi-jurisdiction assets. We have seen certain insurers limiting cover for perceived gaps in due diligence scopes, driven by condensed diligence processes and increased claims activity. However, several insurers continue to offer strong coverage by keeping materiality and a desire to achieve commercial outcomes at the forefront of their underwriting process.

Future Considerations

• We expect an increase in deal volumes in the secondary markets over the next 12 months as investors look to deploy capital outside the primary M&A market to diversify risk.

• We expect an increase in investment in traditionally “recession proof” industries including healthcare, food and consumer staples, and therefore competition for assets, to continue in line with the current economic downturn.

• Early engagement to ring-fence known issues on seller-initiated auction processes ahead of the customary increase in deal volumes towards the end of the year will remain important.