Our solutions

At HWF we believe in a solution-led approach to meet clients’ needs. Please click on the below for information on some of the solutions that we provide.

Our range of transactional insurance products

Warranty & Indemnity Insurance

Insured party:

Buyer or seller.

Policy period:

Typically 2 years for general warranties and 7 years for tax and title exposures.

Coverage:

Protects the insured against financial losses resulting from unknown and unforeseen issues which trigger breaches of the warranties or claims under the tax indemnity given in a SPA.

€500m - €1bn

| Policy type | Buy-Side W&I |

| Sector | Renewable Energy |

| Sellers jurisdiction | UK |

| Target jurisdiction | Ireland |

| Buyers location | Japan |

| Buyer type | Corporate |

Thought leadership

Tax Liability

Insured party:

Buyer, seller, target or other entity if non-M&A related.

Policy period:

Typically follows the statute of limitations up to a maximum of 10 years.

Coverage:

Protects the insured against an adverse ruling by a tax authority. Cover is provided for a broad spectrum of tax issues which often arise as a result of the tax treatment of an M&A transaction, ordinary course operations of the business or previous restructurings, divestments or reorganisations.

£500m - £1bn

| Policy type | Specific Tax liability |

| Sector | Construction |

| Sellers jurisdiction | UK |

| Target jurisdiction | UK |

| Buyers location | France |

| Buyer type | Corporate |

Thought leadership

Contingent liabilities

What is ‘contingent risk insurance’?

Contingent risk insurance covers risks that are known – such as pending or issued litigation, a potential or actual regulatory issue or challenges arising from a re-organisation or a restructuring.

Typically, an insurer will require that the known risk is quantifiable and capable of legal assessment. Generally, contingent insurance works best in scenarios where the risk is remote (making it insurable) but the potential business impact is severe (making insurance an attractive option for the insured). Pricing is highly bespoke, but typically falls within the range of 2% – 10% of the limit of insurance.

Why use it?

Clients have often utilised contingent insurance to unlock transactions, such as M&A and finance deals, that may otherwise have been derailed

by the known risk. Insurance is often a cheaper and more efficient risk transfer mechanism compared to other options, such as a price-chip,

indemnity, escrow arrangements or expensive third-party security. Increasingly, contingent risk insurance is also being deployed outside

of the transactional context. For example, to allow a contingent liability or asset balance sheet provision to be released, allowing dormant cash

to be utilised and recycled through a business. In this way, contingent insurance is helping clients to unlock upside as well as mitigate downside risk.

In a very wide range of settings, we advise clients on contingent risk insurance solutions designed to meet a variety of challenges, including:

Disputes

We structure contingent insurance solutions for disputes that are either active, threatened or which have the potential to emerge in the future.

Appeals

A business may have been successful in a dispute, but that result could be overturned on appeal. A judgment preservation insurance policy “locks-in” the successful outcome, allowing the business to be sold and/or release accounting provisions connected to the dispute.

Contractual Uncertainty

Contingent insurance can provide a safety net where contractual provisions do not provide sufficient certainty – for example, a buyer may lack confidence that it can rely upon a chain of indemnities purportedly in favour of the target.

Insolvency

We arrange insurance that protects insolvency practitioners, creditors and other stakeholders involved in the winding up of an insolvent estate against the risk of third-party claims.

Pensions

Buyers can have concerns regarding their liability to fund very significant pension liabilities – a well-crafted contingent insurance policy can mitigate such risks.

Environmental

Cover for specific environmental liabilities (including known pollution and remediation liabilities).

Re-Classification

A renewables target may be at risk of reclassification such that the preferential price it receives for selling energy would be lost. Such risks, which often turn on a legal issue, are insured with growing frequency.

Potential Tax Issues

Cover for tax risks on M&A transactions, refinancing and restructuring.

Title

Cover for ownership risks including on M&A, real estate and infrastructure transactions.

IP

Contingent insurance can be deployed to cover a range of risks, including infringement claims, non-use trade mark revocation and potential gaps in IP assignments.

Restructuring

Reorganisations can shed light on a range of debt, company and other legal risks that can be addressed by a contingent insurance policy.

Thought leadership

Legal Assets Insurance (Disputes)

Adverse Costs Insurance

We have extensive experience of arranging adverse costs insurance for litigation and arbitration disputes and work with all insurers in the market to secure the most competitive cover.

Judgment Preservation Insurance (JPI)

JPI safeguards returns arising from a successful judgment or award. Allows a claimant or funder to “lock-in” the upside of a case-win – if it is overturned on an appeal the policy will pay out.

Capital Protection Insurance (CPI)

CPI will pay out if a litigation fund’s net returns are, at the conclusion of the fund’s term, less than the capital it has deployed. Can be structured pre or post deployment, on a single or multi-case basis and for all or a portion of deployed capital.

WIP Insurance

WIP insurance covers a law firm for the non-recovery of its fees following an unsuccessful outcome in litigation or arbitration where the firm was acting on a contingent fee arrangement. Cover is available for single cases or a portfolio of matters.

Arbitration Award Default Insurance

Guarantees payment of a legally enforceable arbitral award against a sovereign entity within an agreed timeframe following the sovereign’s failure to honour it.

Cross-Undertaking In Damages

Where a party is required to make a cross-undertaking in damages, we can arrange insurance to satisfy the terms of the court ordered cross-undertaking.

Environmental

Insured party:

Buyer, seller, target or other entity if non-M&A related.

Policy period:

Can be annually renewable or for a fixed period from 1 to 10 years depending on the nature of the risks.

Coverage:

Insurance can be used to offset the risks associated with specific known and unknown liabilities. These may be historic, ongoing or future liabilities. The policy can either back an indemnity or insure the underlying issue directly.

For insurance to be a viable option environmental due diligence should have been undertaken to allow the insurers to assess the level of exposure and for HWF to advise on the most appropriate solution.

€1bn+

| Policy type | EIL Policy (Historic and future pollution) |

| Sector | Manufacturing / Industrials |

| Sellers jurisdiction | Germany |

| Target jurisdiction | Worldwide sites |

| Buyers location | UK |

| Buyer type | Private Equity |

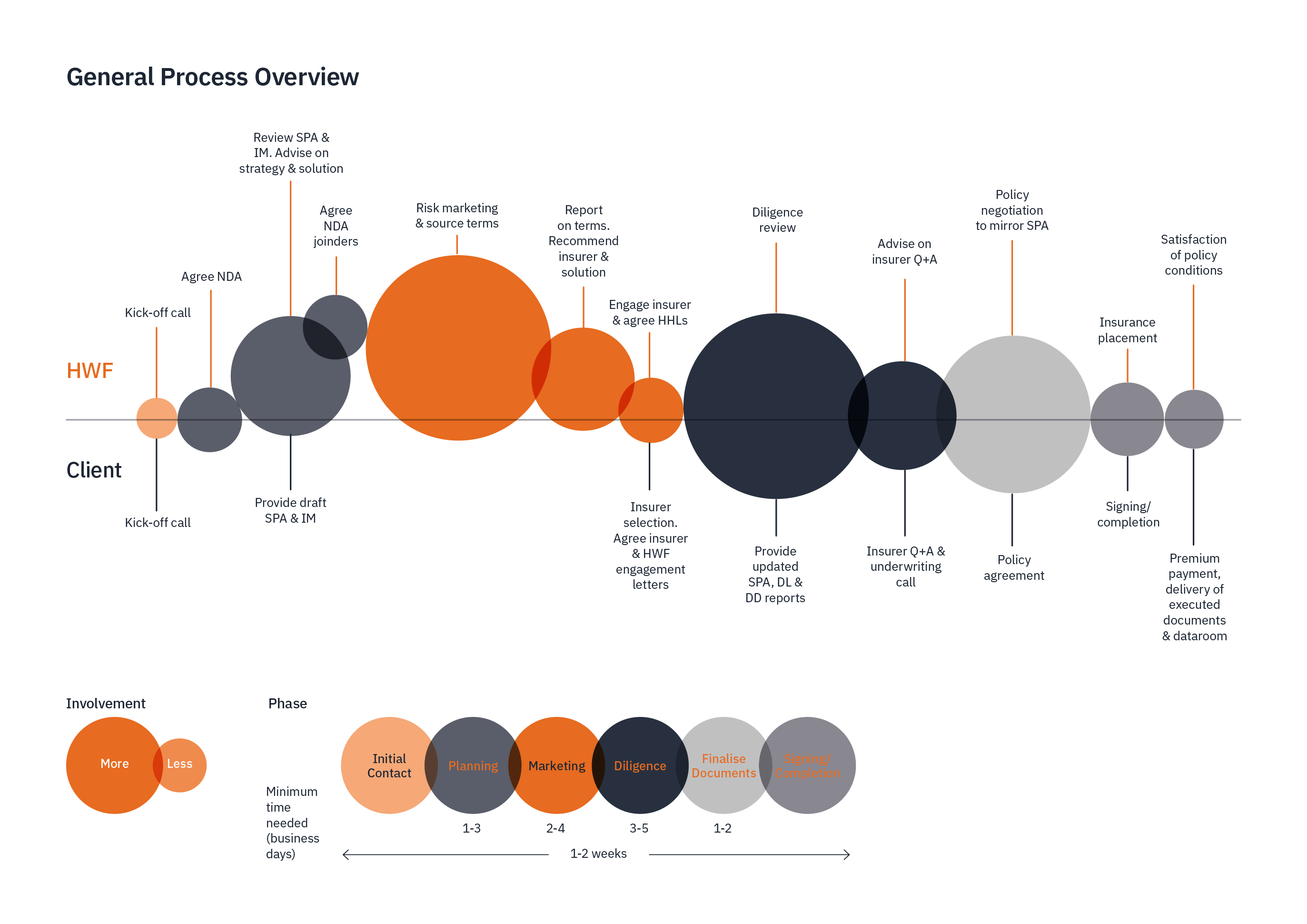

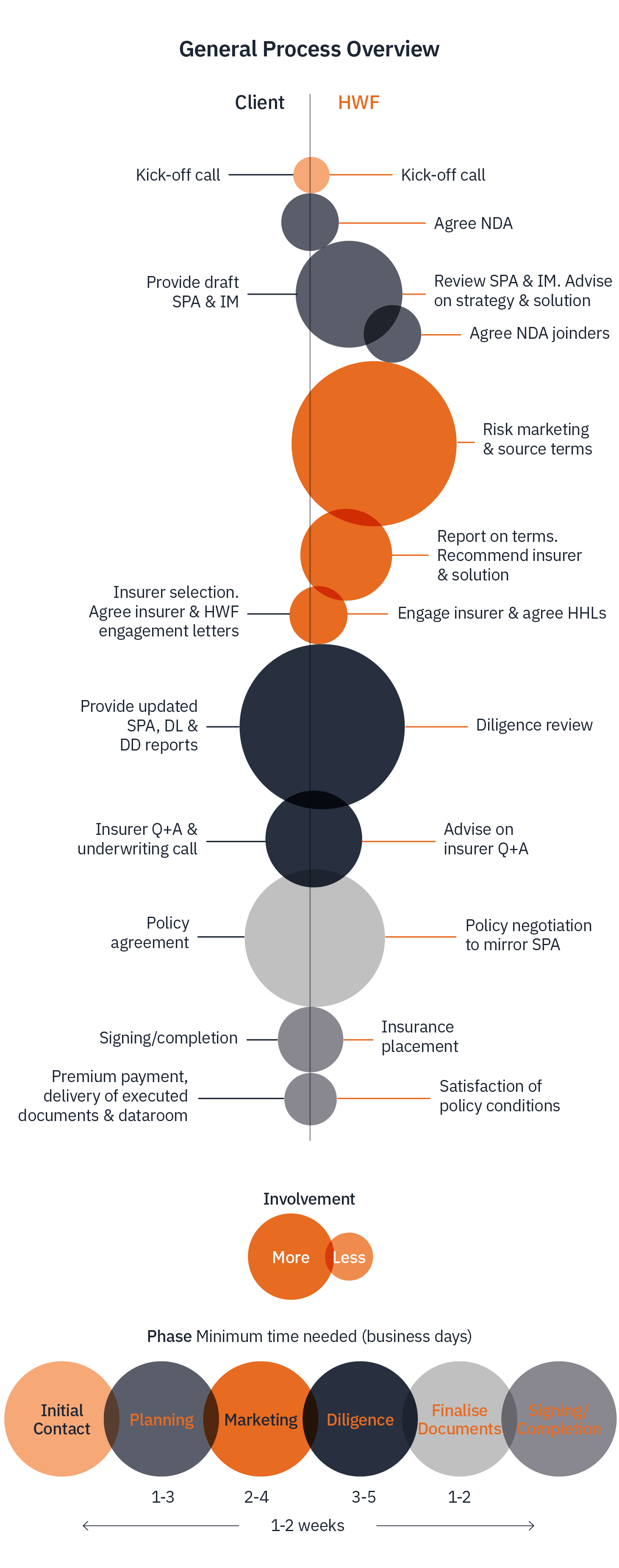

Our process timeline

There are a number of stages involved in the securing of insurance terms and the placement of an insurance policy. The key aspects of each stage are below.

This diagram is based upon a typical W&I insurance solution for an M&A transaction and it should be noted that this will always be tailored to the specific requirements of each transaction.