M&A Insurance: PE Quarterly Market Update – Q1 2023

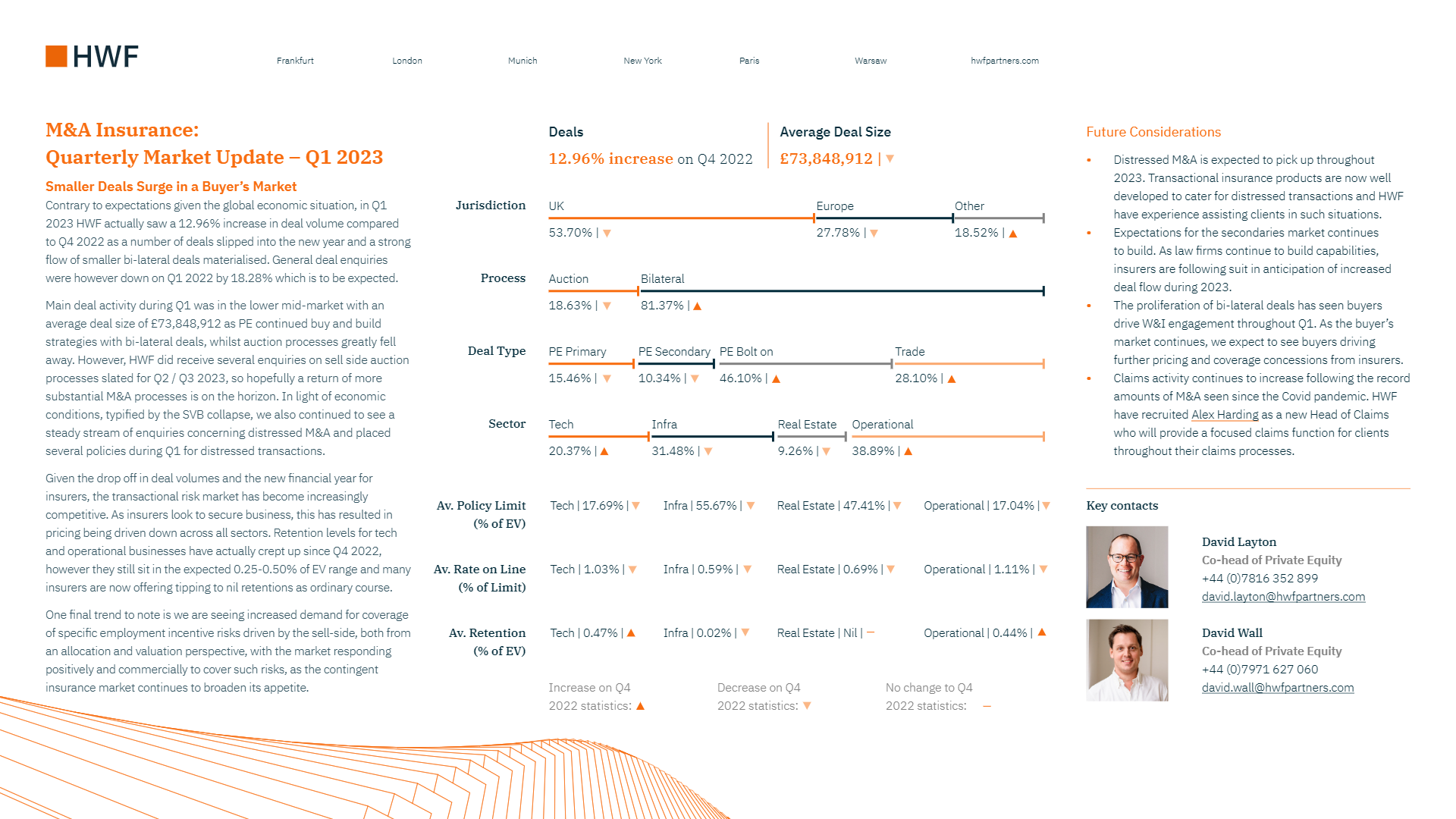

Contrary to expectations given the global economic situation, in Q1 2023 HWF actually saw a 12.96% increase in deal volume compared to Q4 2022 as a number of deals slipped into the new year and a strong flow of smaller bi-lateral deals materialised. General deal enquiries were however down on Q1 2022 by 18.28% which is to be expected.

Smaller Deals Surge in a Buyer’s Market

Main deal activity during Q1 was in the lower mid-market with an average deal size of £73,848,912 as PE continued buy and build strategies with bi-lateral deals, whilst auction processes greatly fell away. However, HWF did receive several enquiries on sell side auction processes slated for Q2 / Q3 2023, so hopefully a return of more substantial M&A processes is on the horizon. In light of economic conditions, typified by the SVB collapse, we also continued to see a steady stream of enquiries concerning distressed M&A and placed several policies during Q1 for distressed transactions.

Given the drop off in deal volumes and the new financial year for insurers, the transactional risk market has become increasingly competitive. As insurers look to secure business, this has resulted in pricing being driven down across all sectors. Retention levels for tech and operational businesses have actually crept up since Q4 2022, however they still sit in the expected 0.25-0.50% of EV range and many insurers are now offering tipping to nil retentions as ordinary course.

One final trend to note is we are seeing increased demand for coverage of specific employment incentive risks driven by the sell-side, both from an allocation and valuation perspective, with the market responding positively and commercially to cover such risks, as the contingent insurance market continues to broaden its appetite.

Future Considerations

- Distressed M&A is expected to pick up throughout 2023. Transactional insurance products are now well developed to cater for distressed transactions and HWF have experience assisting clients in such situations.

- Expectations for the secondaries market continues to build. As law firms continue to build capabilities, insurers are following suit in anticipation of increased deal flow during 2023.

- The proliferation of bi-lateral deals has seen buyers drive W&I engagement throughout Q1. As the buyer’s market continues, we expect to see buyers driving further pricing and coverage concessions from insurers.

- Claims activity continues to increase following the record amounts of M&A seen since the Covid pandemic. HWF have recruited Alex Harding as a new Head of Claims who will provide a focused claims function for clients throughout their claims processes.