COVID-19 and W&I Insurance: Due Diligence and Key Underwriting Considerations

Against the background of the current Covid-19 crisis and its global impact on markets and business operations, W&I insurers now expect buyers to carry out specific due diligence on all areas which might be or have been affected by the pandemic (in addition to the traditional due diligence requirements) and which are covered in the warranties in the SPA.

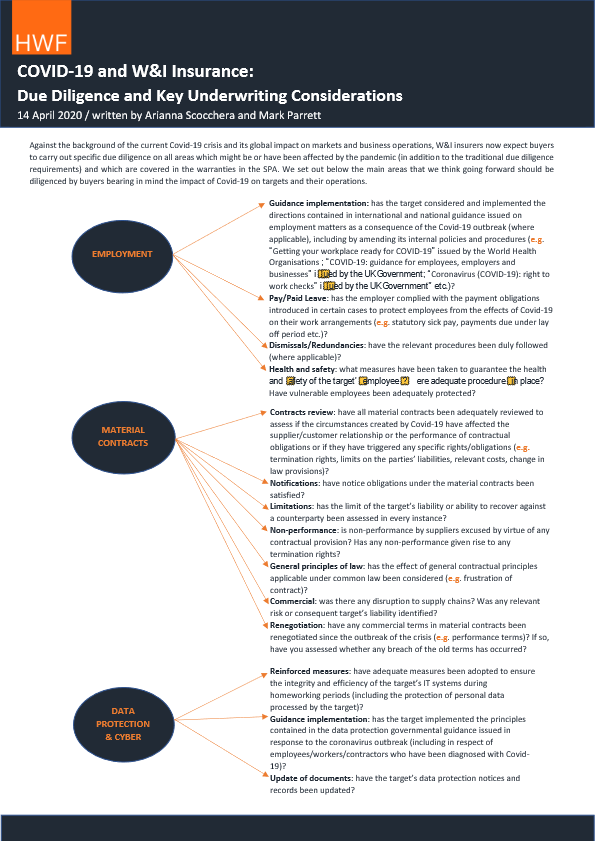

Against the background of the current Covid-19 crisis and its global impact on markets and business operations, W&I insurers now expect buyers to carry out specific due diligence on all areas which might be or have been affected by the pandemic (in addition to the traditional due diligence requirements) and which are covered in the warranties in the SPA. We set out below the main areas that we think going forward should be diligenced by buyers bearing in mind the impact of Covid-19 on targets and their operations.

EMPLOYMENT

Guidance implementation: has the target considered and implemented the directions contained in international and national guidance issued on employment matters as a consequence of the Covid-19 outbreak (where applicable), including by amending its internal policies and procedures (e.g. “Getting your workplace ready for COVID-19” issued by the World Health Organisations ; “COVID-19: guidance for employees, employers and businesses” issued by the UK Government; “Coronavirus (COVID-19): right to work checks” issued by the UK Government” etc.)?

Pay/Paid Leave: has the employer complied with the payment obligations introduced in certain cases to protect employees from the effects of Covid-19 on their work arrangements (e.g. statutory sick pay, payments due under lay off period etc.)?

Dismissals/Redundancies: have the relevant procedures been duly followed (where applicable)?

Health and safety: what measures have been taken to guarantee the health and safety of the target’s employees? Were adequate procedures in place? Have vulnerable employees been adequately protected?

MATERIAL CONTRACTS

Contracts review: have all material contracts been adequately reviewed to assess if the circumstances created by Covid 19 have affected the supplier/customer relationship or the performance of contractual obligations or if they have triggered any specific rights/obligations e.g. termination rights, limits on the parties’ liabilities, relevant costs, change in law provisions)?

Notifications: have notice obligations under the material contracts beensatisfied?

Limitations: has the limit of the target’s liability or ability to recover against a counterparty been assessed in every instance?

Non performance: is non performance by suppliers excused by virtue of any contractual provision? Has any non performance given rise to any termination rights?

General principles of law: has the effect of general contractual principles applicable under common law been considered ( e.g . frustration of contract)

Commercial: was there any disruption to supply chains? Was any relevant risk or consequent target’s liability identified?

Renegotiation: have any commercial terms in material contracts been renegotiated since the outbreak of the crisis ( e.g . performance terms)? If so, have you assessed whether any breach of the old terms has occurred?

DATA PROTECTION & CYBER

Reinforced measures: have adequate measures been adopted to ensure the integrity and efficiency of the target’s IT systems during homeworking periods (including the protection of personal data processed by the target)?

Guidance implementation: has the target implemented the principles contained in the data protection governmental guidance issued in response to the coronavirus outbreak (including in respect of employees/workers/contractors who have been diagnosed with Covid-19)?

Update of documents: have the target’s data protection notices and records been updated?

VALUATION AND CONSIDERATION

Importance of valuation model: understanding the valuation method applied by the buyer in determining the purchase price of the target is of utmost importance for W&I insurers as, in a claim scenario, this will assist in determining the amount of loss recoverable under the policy. Due to the impact of Covid-19, underwriters will seek more details on what valuation method was used, what assumptions were made when using the method, and how (if at all) the impact of Covid-19 was factored into the valuation.

It will be important to show that consideration has been given to:

– the size of the Covid-19 impact and length of time such impact has had and is expected to have on the target;

– the treatment of debts and how easily these will be able to be turned into cash;

– what cost savings and deferrals could be made; and

– what help the Government is providing to the target.

Regardless of any mitigating factors, there is likely to be a shift in balance in the M&A market with buyers being able to acquire businesses for less than they would have prior to the pandemic. While this should be a positive for insurers, where valuations go down significantly insurers could find themselves insuring a large business from an assets perspective for a low value and find themselves with greater exposure.

Consideration structure in SPAs: Covid-19 is expected to influence the way buyers will structure the mechanisms of payment of the deal consideration under the SPAs. Due to the uncertainty of the future performance of businesses, it is likely that earn-out and completion adjustment mechanisms will be more frequently used than the pre-Covid-19 most commonly used locked-box structure. W&I insurers will expect buyers to be able to explain the rationale behind the choice of a specific consideration structure and the relation between the valuation model and such structure.

TAX

Maintenance of tax residency: have the board meetings taken place in the country of tax residence and were a sufficient number of non resident directors able to attend in person?

Creation of permanent establishments: where key employees have returned to their country of origin, has t heir remote working inadvertently created a taxable presence for the company in another jurisdiction?

Usage of tax assets: where, for example, losses generated during reduced trading have been carried back against prior year profits, are these assets sufficiently robust and will they survive change in ownership rules that look back pre completion?

Deferral of tax payments: where companies have taken advantage of tax payment deferral schemes, are they carrying appropriate provisions in respect of these deferred tax accruals and is their tax creditor position sufficiently robust?

Reorganisations/debt waivers etc: where groups have undertaken re organisations or waived debts, have these been correctly treated for tax purposes and has appropriate advice been taken?

FINANCE AND CREDIT FACILITIES

Impact on finance and solvency: has the diligence covered the impact of Covid-19 on the target from a financial performance point of view? Has any solvency or other material risk been identified? Have applicable Government subsidies/incentives received by the target and all relevant obligations (e.g. under the Covid-19 Corporate Financing Facility (CCFF), the Coronavirus Business Interruption Loan Scheme (CBILS), or the HMRC Time To Pay Scheme) been taken into account when assessing the target’s financial situation?

Financial arrangements review: have all financing and banking arrangements of the target been reviewed to assess whether the Covid-19 crisis has had an impact on those.

For example:

– was any termination event/right triggered under the arrangement?;

– was there a market disruption clause in the arrangement?;

– was any breach of the arrangement terms or covenants identified and, if so, how material was it?; and

– was the risk of cross-default assessed?

It should be noted that the above is not exhaustive and there are other areas in addition to other items within the categories reviewed hereunder which will be object of the W&I underwriters’ scrutiny from a Covid-19 perspective. Due diligence requirements will also vary depending on the sector in which the target operates. As such, we would always recommend that you contact us early in the process so that we can input into your scope of due diligence to ensure it is sufficient from a W&I perspective.